About 10 years ago I was working as Accenture consultant in Europe on an implementation of common data and processes for Sara Lee. This project was implementing ERP and APS systems across 15 operations companies in 10 countries and must have roughly cost a 100 million Euro. Through a vendor selection model it was decided to use SAP R/3 and the then little mature APO as enabling systems. At that time there were four main criteria and a weighting agreed with the client.

- Partner characteristics (40%)

- Technical characteristics (20%)

- Product/package characteristics (25%)

- Business requirements (15%)

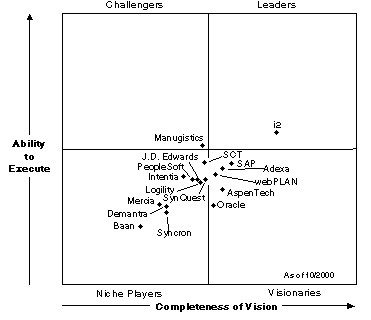

From advanced planning and scheduling (APS) perspective, the shortlist was SAP/APO, Manugistics and i2. As you can see from the 2000 Gartner quadrant from that time, i2 was still seen as the only APS visionary. Interestingly enough, a couple of quarters later during the APS vendor selection, there was no APS visionaries anymore in the Gartner quadrant as SAP put their massive development team behind APO to catch up. The Sara Lee decision board decided that, although the package and functionality from i2 and Manugistics was superior, SAP APO provided a better long term strategic choice due to a stable one partner choice and package integration.

Sara Lee was right to go for the long term view! Ten years later we see that from the 3 dominant APS players 12 years ago (i2, Manugistics, SAP/APO) only SAP is left. i2 and Manugistics both got acquired by JDA. It shows that being a visionary doesn’t mean having a bright future. Maybe that’s the reason that since 2002 the top right box of the Gartner quadrant has been staying empty!

Since then, APS has been imbedded in most medium to large companies who are now looking for the next enablers to further support integrated business processes like S&OP. Who are they turning too? Who are the S&OP visionaries and who would be on the shortlist for a global S&OP system roll out?

Newer solutions like Steelwedge or Kinaxis with cloud based and SAAS solutions and S&OP specific data structures? Or JDA and Oracle who have apparently the Oliver Wight process methodology integrated? Or if you have to spend a lot of money, would you go for SAP with a clunky S&OP solution, but a partner who will most likely still be there in 2022?

I am not sure that staying with SAP APO was necessarily a lower risk or lower TCO choice for Sara Lee. Just because i2 and Manugistics were eventually acquired by JDA does not make selecting i2 as a “poor choice” or “bad future”. The market needed consolidation, and the major acquirers have slowed or “chilled” innovation in this space, and there is now significant pull brewing for newer solution approaches, SaaS or not.

Having gone through the same “supply chain system” selection and implementation process over the past 20 years a number of times at global FMCG companies – from the time where simply nothing was available, over SAP R/3, Numetrix, Manugistics, I2, APO and Kinaxis – I think it safe to say that allmost all of the basic supply chain optimisation requirements can now be found in APO, and are largely sufficient for 80-90% of SAP users. The main advantage of using APO when already an SAP user are the reliability of, and a single supplier, which, to many larger companies is a strategic choice (“integration” between SAP-ERP and APO is relative).

The choice of a more advanced solution should be based on : 1. unique process requirements, only available in a “standard” software configuration of a specific supplier (customization being justified in only very rare cases where they really deliver a competitive advantage). 2. payback of the investment in service level, inventories or cost (e.g. chosing Manugistics 15 years ago, with a 3 year payback, has proven an excellent choice – once these results achieved however, changing to another provider or technology becomes a lot more difficult, unless there is significant innovation to justify another step change in KPI. As such it has taken Kraft Foods 12 years to eventually be able to justify a change from Manugistics to APO).

At this point in time – anno 2012 – no single supplier “stands out”. And rightfully so, there are no true S&OP visionaries. Are supply chain gurus out of ideas ? Or is the bulk of the business/companies still so far “behind” that we can go on with what is out there for quite a while longer ?